Mortgage Credit Score vs Consumer Credit Score: What's the Difference?

You have a credit score — probably more than one. But when it comes to buying a home, which one actually matters?

The answer is your mortgage credit score, and there's a good chance it looks different from anything you've seen on a free monitoring platform. Understanding why these scores differ — and what drives each one — is one of the most practical things a prospective home buyer in Jacksonville, FL can know before stepping into the mortgage process.

Two Different Tools Built for Two Different Purposes

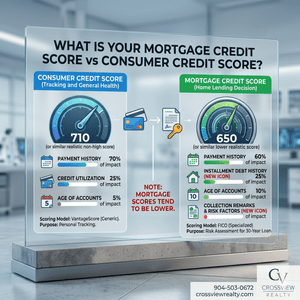

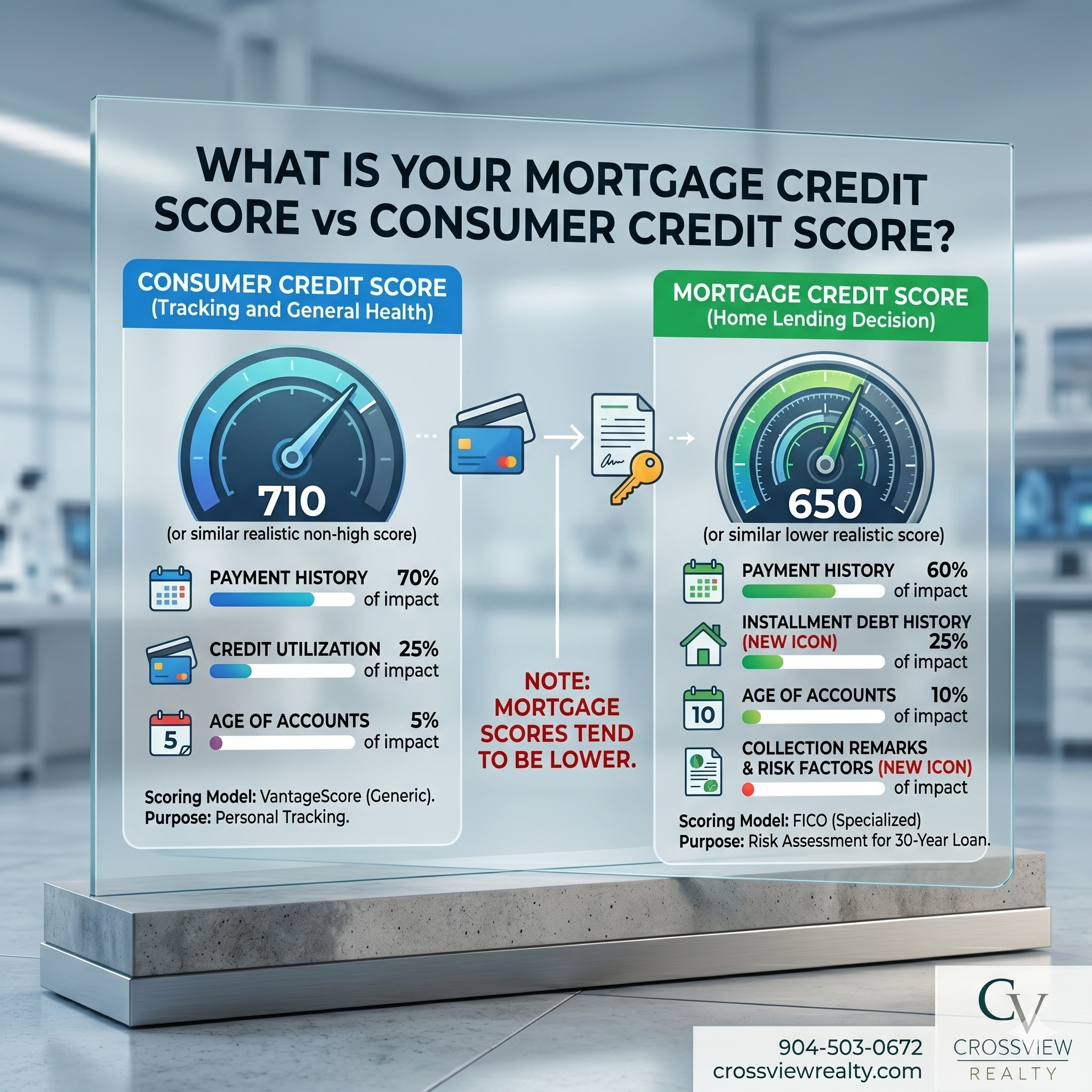

Consumer credit scores — the kind you see on Credit Karma, your bank's app, or other free platforms — are designed to give you a general snapshot of your credit health. They're useful for tracking trends, catching errors, and getting a broad sense of where you stand. The most common model behind these scores is the VantageScore, developed collaboratively by the three major credit bureaus.

Mortgage credit scores use a different model entirely. Lenders who issue home loans are required to use specific versions of FICO scores — and they pull all three bureaus separately, then typically use the middle score to make lending decisions. The FICO models used in mortgage lending are built specifically to predict the likelihood of a borrower defaulting on a home loan. That's a very different question than "how creditworthy is this person in general?" — and it produces a different answer.

Same credit file. Different lens. Different score.

How the Weighting Differs

Both scoring models look at the same basic categories — payment history, amounts owed, length of credit history, types of credit, and new credit. But the weight each model assigns to those categories varies, and that's where the scores start to diverge.

Mortgage scoring models tend to place significant emphasis on how you've handled large, long-term installment debt — because that history is the most predictive of how you'll handle a 30-year mortgage. Your overall debt load relative to your income, any past delinquencies, and the age and diversity of your credit accounts all factor in, sometimes more heavily than they would in a consumer score calculation.

When you apply for a car loan or finance furniture, the lender pulling your credit is using a model calibrated for that type of lending — shorter term, smaller balance, different risk profile. The score that comes back reflects what matters for that transaction. A mortgage lender's model reflects what matters for theirs.

Why Mortgage Scores Tend to Run Lower

For most buyers we work with across the Jacksonville and Northeast Florida market, the mortgage credit score comes in lower than what they've been tracking online. Sometimes it's a modest gap. Sometimes it's more significant. Either way, it's rarely the number they expected.

This isn't a flaw in the system — it's the system working as designed. Mortgage lending carries more risk and longer time horizons than most other consumer lending, so the scoring model is more conservative. It's calibrated to identify risk that a general consumer score might not flag as prominently.

The practical takeaway: don't plan your home purchase around the number on your phone. Plan it around the number a lender gives you.

What Buyers in Northeast Florida Should Do With This Information

First — don't make changes to your credit before talking to a lender. This is critical. Moves that improve a VantageScore don't always improve a mortgage FICO score, and in some cases they do the opposite. Paying off a collection account, closing a card, opening new credit — any of these can have unintended consequences on your mortgage score specifically. We've seen buyers hurt their own position by trying to help it.

Second — get your mortgage credit score pulled early. Not when you're ready to make an offer. Before you even start seriously touring homes in Orange Park, Ponte Vedra Beach, St. Augustine, or anywhere across St. Johns County. Knowing your actual number gives you time to work on it strategically, with professional guidance, if needed.

Third — lean on a lender who can advise you specifically. A good mortgage professional doesn't just tell you your score — they tell you what's driving it, what to address first, and what to leave alone. That kind of specific, file-level guidance is worth far more than anything you'll find in a general article.

If you need help finding the right lender for your situation, CrossView Realty is happy to make a connection. We work with strong lending partners across Northeast Florida, and the right fit varies depending on your goals, timeline, and credit profile.

Have questions about where to start on your home buying journey in Jacksonville, FL? Give us a call at 904-503-0672, email us at info@crossviewrealty.com, or visit crossviewrealty.com. We'll help you get connected with the right people from the very beginning.

Frequently Asked Questions

Q: What's the difference between a mortgage credit score and a consumer credit score? Consumer credit scores — like those from Credit Karma — use the VantageScore model and are designed to reflect general credit health. Mortgage credit scores use specific FICO models required by home lenders, which weight credit factors differently because they're predicting the risk of defaulting on a long-term home loan. The same credit file can produce meaningfully different numbers under each model.

Q: Why does my mortgage credit score come in lower than my Credit Karma score? Mortgage FICO models are more conservative by design. They're calibrated to assess risk over a long repayment period — like a 30-year mortgage — and tend to place heavier weight on factors like installment loan history and overall debt load. That conservative lens often produces a lower number than what consumer-facing scoring models return.

Q: Can I improve my mortgage credit score before buying a home in Jacksonville, FL? Yes, but only strategically and with guidance from a mortgage lender. What works for a consumer score doesn't always work for a mortgage score — and some common fixes can actually lower your mortgage score. Have a lender pull your actual score first, then follow their specific recommendations for your credit file before making any changes.

Q: Should I check my credit score before talking to a mortgage lender? It's fine to check, but don't rely on it for planning purposes. Checking your own score is a soft inquiry and won't hurt you. Just know that the number you see is likely different from your mortgage credit score. The real starting point is having a lender pull your mortgage-specific score so you're working with accurate information from day one.