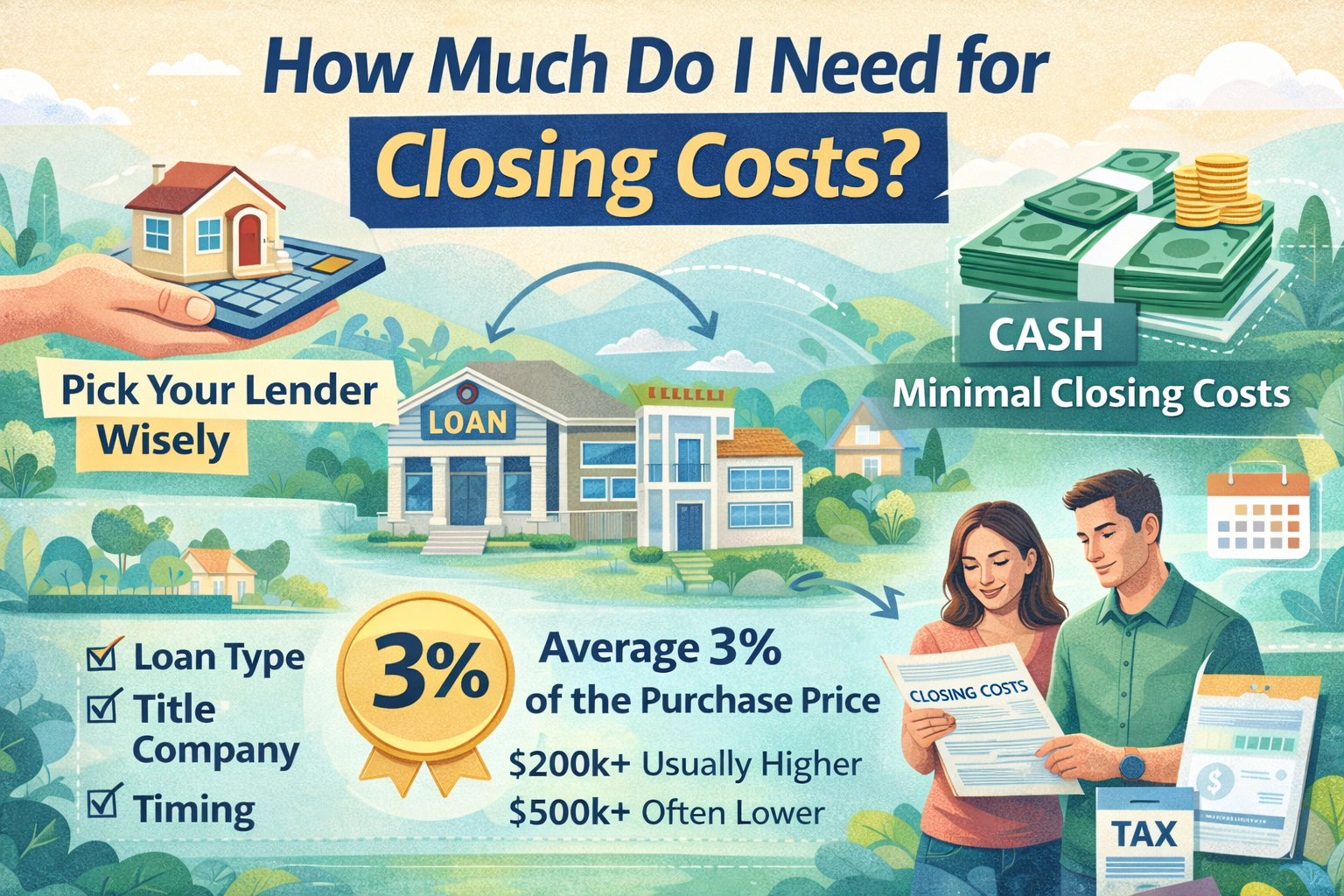

How Much Do I Need for Closing Costs?

How much do you actually need for closing costs when buying a home?

The short answer is: it depends — and the range can be wide.

But there are some solid guidelines that can help you plan without being surprised at the closing table.

Let’s break it down in a way that actually makes sense.

First, What Are “Closing Costs”?

When we talk about closing costs here, we’re not talking about agent commissions.

We’re talking about the actual costs associated with closing the transaction:

Lender fees

Title-related costs

Prepaid items like taxes and insurance

Prorations

Cash Buyers: The Simplest Scenario

If you’re paying cash, your closing costs are very minimal.

Most closing costs are tied to loans — so without a loan:

No lender fees

No prepaid interest

No loan-related costs

You’ll still have some title-related expenses, but overall, cash buyers have the lowest closing costs by far.

For Buyers Using a Loan: The Lender Matters (A Lot)

If you’re getting a mortgage, the lender you choose plays a huge role in your closing costs.

Over the years, lenders have gotten very creative with how they present fees.

You may hear:

“We don’t charge a loan origination fee.”

That doesn’t always mean the loan is cheaper.

Often, that fee is simply:

Renamed

Broken into smaller fees

Or offset by higher costs elsewhere

The money doesn’t disappear — it just moves around.

Some lenders are genuinely more competitive than others, which is why it’s so important to:

Shop around

Compare loan estimates

Get more than one opinion

Please don’t just go with the first lender you talk to.

Title Company Fees Can Vary

Another piece that impacts closing costs is the title company.

Some title companies:

Charge both the buyer and the seller a closing fee

Others:

Only charge the seller

If you’re not picking the title company, you won’t know which one the seller chooses — so it’s smart to leave a little buffer.

A good estimate is:

$200–$450 for potential buyer-side title fees

Timing Matters More Than You Think

When you close can change your closing costs.

Time of Year

Taxes, HOA fees, condo fees, and CDD fees are all prorated based on the time of year you close.

Time of Month

Early in the month: Higher closing costs, but your first mortgage payment is farther away

End of the month: Lower closing costs, but your first payment comes sooner

Either way, you’re paying — it’s just when you pay it that changes.

A Good Rule of Thumb: 3%

If you want a safe planning number, a solid estimate is:

👉 About 3% of the purchase price

But there are exceptions:

Under $200,000: Often more than 3%

Over $500,000: Often less than 3%

This does not include:

Rate buy-downs

Additional points paid to lower your interest rate

Those would be extra on top of that estimate.

Final Takeaway

Closing costs are influenced by:

Loan type

Purchase price

Lender fees

Title company

Time of year

Time of month

That’s why the range can feel confusing.

If you’re planning on buying, the best thing you can do is:

Ask questions

Compare lenders

Read your loan estimates carefully

At CrossView Realty, we spend a lot of time helping buyers understand what they’re signing and what to expect financially.

If you’d like lender recommendations based on buyers we’ve worked with before, we’re happy to share — and you’re always free to use whoever you choose.

If you have questions or want help planning ahead, give CrossView Realty a call at 904-503-0672 or email info@crossviewrealty.com. We’re here to educate and help you feel confident every step of the way.